Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Unlocking the Secrets of the North Reading, MA

**Unlocking the Secrets of the North Reading, MA 01864 Real Estate Market: A Deep Dive into the Numbers**

If you’re considering entering the real estate market in North Reading, Massachusetts, you’re in for a dynamic journey. The picturesque town, known for its charming neighborhoods and excellent school system, is currently experiencing intriguing trends that savvy buyers and sellers should take note of.

**Current Market Snapshot: Single Family Listings**

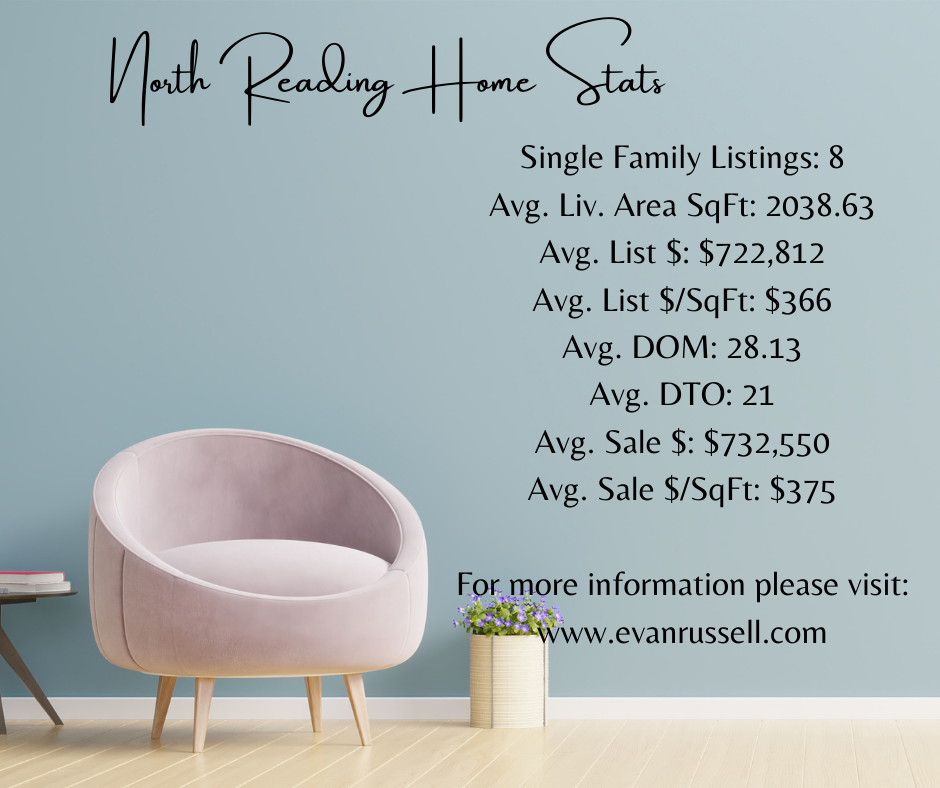

As of November ’23, North Reading boasts a total of 8 single-family listings, offering a snapshot of the town’s housing inventory. These homes vary in size, style, and amenities, contributing to the diverse options available to potential buyers.

**Size Matters: Average Living Area SqFt**

Buyers looking for spacious homes will be pleased to note that the average living area of listed homes in North Reading is approximately 2038.63 square feet. This suggests a preference for roomy residences, catering to the needs of families and individuals alike.

**Setting the Price: Average List Price**

For those curious about the financial aspect, the average list price in North Reading stands at $722,812. This figure is reflective of the town’s desirability and the quality of homes available. It’s essential to note that this average encompasses the entire range of homes on the market, from cozy bungalows to luxurious estates.

**Breaking it Down: Average List Price per Square Foot**

Delving further into the pricing dynamics, the average list price per square foot is $366. This metric provides insights into how the market values space within a home. It’s a critical factor for both buyers and sellers, helping them understand the relative value of different-sized properties.

**Timing is Key: Average Days on Market (DOM) and Average Days to Offer (DTO)**

The North Reading real estate market moves at a steady pace. On average, homes spend approximately 28.13 days on the market before attracting an offer. The average days to offer (DTO) is even more impressive, standing at 21 days. These figures underscore the town’s appeal and the efficiency of its real estate transactions.

**What Homes Are Selling For: Average Sale Price**

For those with an eye on the bottom line, the average sale price in North Reading is $732,550. This provides valuable insights for sellers looking to set a competitive yet realistic asking price and for buyers assessing their budget and negotiating power.

**Dollars and Sense: Average Sale Price per Square Foot**

Analyzing the data from another perspective, the average sale price per square foot is $375. This metric further refines the understanding of property values, assisting both buyers and sellers in making informed decisions.

**Conclusion: Navigating the North Reading Real Estate Landscape**

As North Reading, MA, continues to draw interest from homebuyers, understanding the market trends becomes paramount. With an average list price of $722,812 and an efficient sales cycle, the town offers a promising real estate landscape. Whether you’re a buyer seeking the perfect home or a seller looking to make a smart move, these statistics provide valuable insights into the dynamics of the North Reading real estate market. Stay tuned for updates as this vibrant market evolves, and opportunities unfold.

September ’23 Market Trends for North Reading

Title: “Exploring the Real Estate Landscape in North Reading’s 01864 Zip Code”*

Are you considering buying or selling a single-family home in North Reading’s 01864 zip code? If so, you’re in the right place. This picturesque town, located in Middlesex County, Massachusetts, has a lot to offer to both homebuyers and sellers. In this blog post, we’ll dive into the current real estate market stats for North Reading’s 01864 zip code to give you a better understanding of what’s happening in the area.

**1. Abundant Choices for Single Family Homes**

As of the latest data available, there are 10 single-family homes listed in the 01864 zip code. This means that potential buyers have a decent selection to choose from, ensuring there’s something for everyone’s tastes and preferences.

**2. Spacious Living Areas**

The average living area square footage for these single-family homes is an impressive 2,581.9 square feet. This spaciousness provides ample room for families to grow, entertain, and enjoy their living spaces comfortably.

**3. Competitive Listing Prices**

The average list price for homes in North Reading’s 01864 zip code stands at $865,170. This figure provides a reasonable starting point for negotiations and gives buyers and sellers alike a sense of the local market’s pricing trends.

**4. Price Per Square Foot**

For those who like to dig deeper into the numbers, the average list price per square foot comes in at $367. This metric can be particularly useful for comparing the relative value of different properties and understanding how much space you’re getting for your money.

**5. Quick Turnaround**

On average, homes in this area spend approximately 16.8 days on the market (DOM) before finding their new owners. This relatively short timeframe suggests that the market is active and that desirable properties are moving quickly.

**6. Swift Sales**

Once a property goes under contract, it typically takes just 9 days on average for it to close. This “days to offer” (DTO) metric highlights the efficiency of the local real estate transactions, ensuring that buyers and sellers can wrap up their deals in a timely manner.

**7. Strong Sale Prices**

The average sale price for homes in North Reading’s 01864 zip code comes in at a robust $879,300. This figure reflects the actual market value of properties in the area and can help sellers set realistic expectations for their homes’ final sale prices.

**8. Price Per Square Foot at Sale**

For those interested in the price per square foot at the time of sale, the average is $372. This number illustrates how much buyers are willing to pay for each square foot of living space, providing valuable insights into the market’s demand.

In conclusion, North Reading’s 01864 zip code offers a dynamic real estate market with a variety of single-family homes, spacious living areas, and competitive pricing. With homes selling relatively quickly and at strong prices, it’s an exciting time for both buyers and sellers in this charming Massachusetts town. If you’re considering a move to North Reading or planning to sell your property here, these market stats should give you a solid starting point for your real estate journey. Remember to work with a knowledgeable local real estate agent to navigate this vibrant market successfully.

Home Market Report: A Thriving Real Estate Market in 2023

Reading, MA 01867 Home Market Report: A Thriving Real Estate Market in 2023

Welcome to our comprehensive home market report for Reading, MA 01867! Whether you’re a prospective homebuyer, a seller, or simply interested in the local real estate trends, this report will provide you with valuable insights into the current state of the housing market in Reading, Massachusetts. With its charming neighborhoods, excellent schools, and convenient location, Reading offers an attractive living environment for residents. Let’s delve into the statistical data and explore the key factors driving the market in Reading.

The real estate market in Reading, MA 01867 is thriving, with a diverse range of single-family listings available for buyers. In this report, we will analyze the average living area square footage, listing prices, days on market (DOM), and other important metrics to give you a comprehensive understanding of the current market trends.

Key Market Statistics:

1. Single Family Listings: Currently, there are 50 single-family listings available in Reading, MA 01867, providing a wide array of choices for prospective buyers.

2. Average Living Area SqFt: The average living area square footage for homes in Reading is approximately 2,565.68 square feet. This generous living space ensures ample room for comfortable family living.

3. Average Listing Price: The average listing price for homes in Reading stands at $968,168. This price range reflects the value and desirability of the properties in the area.

4. Average Listing Price per SqFt: The average listing price per square foot is $390. This metric allows buyers to compare prices between different properties based on their size, ensuring informed decision-making.

5. Average DOM (Days on Market): The average days on market for homes in Reading is approximately 28.96. This indicates that homes are selling relatively quickly, showcasing the high demand for properties in the area.

6. Average DTO (Days to Offer): On average, homes in Reading receive offers within 21.28 days. This highlights the competitiveness of the market and the desirability of properties in the area.

7. Average Sale Price: The average sale price for homes in Reading is $1,005,576. This data showcases the strong market performance and the potential for a solid return on investment.

8. Average Sale Price per SqFt: The average sale price per square foot is $414, demonstrating the appreciation and value of properties in Reading.

Reading, MA 01867 presents an enticing real estate market with its diverse range of single-family listings, generous living spaces, and competitive prices. The average days on market and days to offer figures indicate that the market is dynamic, attracting buyers eager to invest in this vibrant community.

With its beautiful neighborhoods, and convenient location, Reading continues to be a sought-after destination for families and individuals looking for a high quality of life. Whether you’re planning to buy or sell a home, understanding the current market trends is crucial to making informed decisions.

We hope this home market report has provided you with valuable insights into the real estate landscape in Reading, MA 01867. For personalized guidance and assistance with your real estate needs, reach out to a trusted local real estate professional. Happy house hunting or selling!

Helpful Links:

Exploring the North Reading Home Market: A Comprehensive Guide Q2

Title: Exploring the North Reading Home Market: A Comprehensive Guide

Introduction

Are you considering investing in a home in North Reading? With its charming neighborhoods, excellent schools, and convenient location, North Reading has become an attractive destination for homebuyers. In this article, we will delve into the current state of the North Reading home market, providing you with valuable insights and statistics to help you make an informed decision. From average listing prices to days on the market, we will cover key metrics that reflect the market’s health and trends. Let’s dive in!

Understanding the North Reading Home Market

The North Reading home market offers a diverse range of properties, catering to different preferences and budgets. To gain a better understanding of the market, let’s analyze some of the essential statistics:

1. Single Family Listings: 34

– The number of available single-family homes in North Reading currently stands at 34. This figure provides an overview of the housing supply in the area.

2. Average Living Area SqFt: 2,662.74

– The average living area square footage of homes in North Reading is approximately 2,662.74 sq. ft. This measurement indicates the average size of houses available for purchase, offering potential buyers an idea of the space they can expect.

3. Average List Price: $932,435

– The average list price of homes in North Reading is $932,435. This figure represents the typical asking price for properties in the area.

4. Average List Price per SqFt: $377

– The average list price per square foot in North Reading is $377. This metric helps determine the value of the property relative to its size.

5. Average Days on Market (DOM): 26.03

– On average, homes in North Reading spend approximately 26.03 days on the market before being sold. This metric indicates the average time it takes for properties to find buyers.

6. Average Days to Offer (DTO): 10.41

– The average number of days it takes for a home in North Reading to receive an offer is 10.41. This statistic highlights the speed at which potential buyers show interest in available properties.

7. Average Sale Price: $972,544

– The average sale price for homes in North Reading is $972,544. This figure reflects the final price at which properties are typically sold.

8. Average Sale Price per SqFt: $399

– The average sale price per square foot in North Reading is $399. This metric provides insight into the value of properties based on their size.

Key Takeaways

Based on the above statistics, several key takeaways emerge about the North Reading home market:

1. Pricing: The average list price of homes in North Reading is $932,435, while the average sale price is slightly higher at $972,544. This indicates that buyers should be prepared for potential negotiations or price adjustments during the purchasing process.

2. Property Size: With an average living area of approximately 2,662.74 sq. ft., homebuyers can find properties that offer ample space to meet their needs.

3. Market Activity: The average DOM of 26.03 and DTO of 10.41 indicate that the North Reading home market is relatively active, with properties often receiving offers quickly.

4. Market Value: The average list price per square foot is $377, while the average sale price per square foot is $399. These figures suggest that properties in North Reading hold their value well.

Conclusion

The North Reading home market presents a range of opportunities for homebuyers looking for a desirable and convenient location. With an average living area of 2,662.74 sq. ft., ample housing options are available to suit various preferences. While the average list price stands at $932,435, buyers should expect potential negotiations during the purchasing process. The market’s activity level is reflected in the average DOM of 26.03 and DTO of 10.41. Overall, the North Reading home market demonstrates stability and value for potential homeowners.

When exploring the North Reading home market, it’s essential to consult with a qualified real estate agent who can provide personalized guidance and help navigate the buying process. By utilizing the statistics and insights provided in this article, you can make informed decisions and find the perfect home in North Reading. Happy house hunting!